By: Thom Albrecht – Chief Revenue Officer at Reliance Partners

For small and mid-sized motor carriers, especially those with a fair amount of dependence

upon freight brokers and the overall spot market, the trucking recession is now four years

old, having begun in February 2022. Larger carriers, especially enterprise carriers (defined as

those with 3 or more solutions to shippers (examples: OTR, dedicated, intermodal,

brokerage, final mile, etc.), generally didn’t feel the trucking downturn until late summer 2022

or even post Labor Day.

The recovery was only about 2 years, so a 3.5 to 4 year downturn is not only significant, but it

far outpaces previous cycle downturns. On average, the last 4 downturns were about 20%

longer than the previous recoveries.

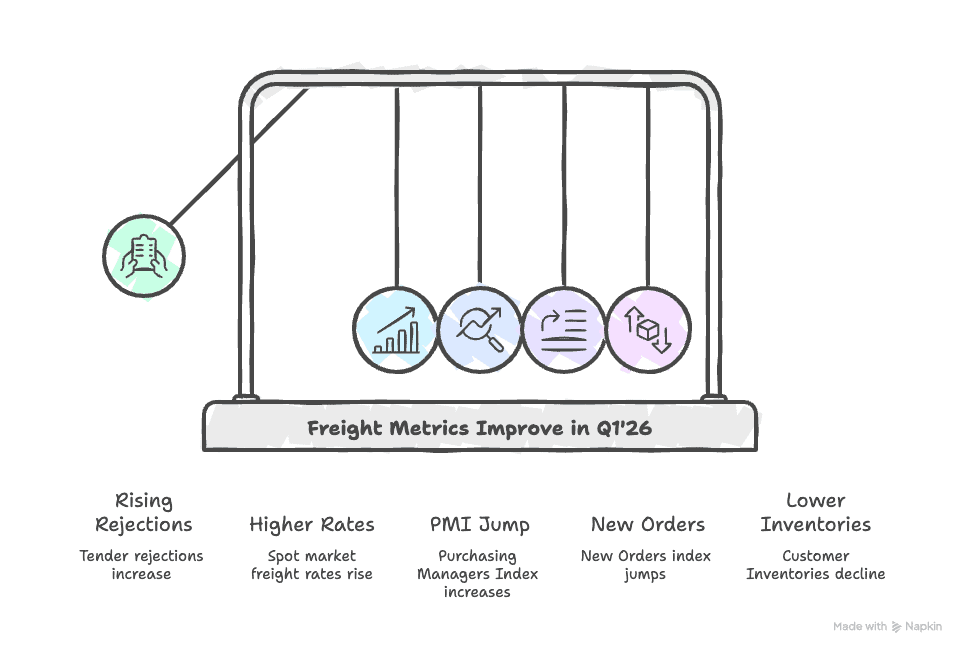

Have Any Important Freight Metrics Actually Improved?

Freight vital signs began to percolate in late November and continued to advance in Q1’26,

most prominently captured in rising first load tender rejection rates and an increase in spot

market freight rates. Depending upon which source one examines, tender rejections have

risen from about 5% to approximately 13% to 14%, while average spot rates are up over 20%,

with many lanes up significantly more.

Adding to the optimism was the Purchasing Managers report, released by ISM on February 3.

The PMI and its 10 sub-indices are momentum measures, with figures above 50.0

representing growth of various elements of manufacturing, while below 50.0 represents

manufacturing contraction. PMI’s 10 sub-indices are categories like exports, imports,

inventories, backlog, production, labor, etc. The PMI index jumped to 52.6 from 47.9, only

the second month above 50.0 in the last 50 months. [Note: not a typo!]

More pertinent to trucking was the nearly 10-point jump in New Orders (from 47.4 in

December to 57.1) and the continued decline in the Customer Inventories (CI) figure

(declined from 43.3 to 38.7). Both are indications of future trucking volumes. On New Orders,

the higher the better for future freight and with Customer Inventories, the lower the number

the better for trucking as this suggests that companies don’t have enough inventories,

meaning additional replenishment orders and truck shipments. The all-time low for CI was

25.0 in July 2021, when trucking was booming. Conversely, CI has been hovering between 45

to 50 for the better part of two years, so a drop below 40 is noteworthy

If 2026 Finally Has a Recovery, Will it be a Demand and a Supply Recovery in

Trucking? Or Just One of Those Two Elements?

Let’s start with a demand discussion. Critical factors impacting demand remain mediocre—if

not pressured. We break it down around 3 influences: a) The health of the consumer, b)

Business confidence, which drives capital spending and industrial production, and c)

Housing trends.

3 Big Buckets Impact Trucking Volumes—How Does 2026 Look?

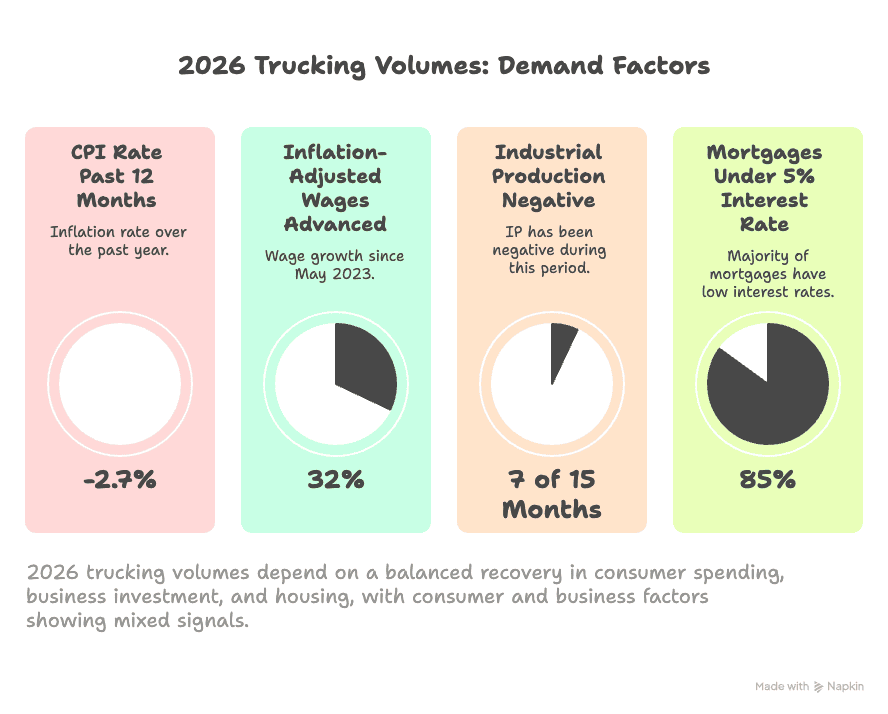

1) The Consumer: For 28 consecutive months from 2021 into mid-2023, inflation-adjusted

wages trailed inflation, meaning month after month consumers lost purchasing power.

Fortunately, since May 2023, inflation-adjusted wages have advanced 32 consecutive

months. However, when consumers lose purchasing power, it can often take twice as

long to regain their purchasing power. And many items, some in the CPI (consumer

price index) and some not reflected in the monthly CPI report have risen significantly

more than the 2.7% CPI rate of the past 12 months. This includes items bought on a

regular basis such as food and beverages, various consumer products, diapers,

coffee, pet food, deodorant and other periodic purchases like car and home owners’

insurance, tax preparation, materials for home repairs, furniture, etc.

Thus, while the consumer is experiencing a recovery in lost purchasing power, it may be midto-

late 2027 before the consumer is described as all the way back and “flush with cash”.

2) Business Spending: This is where it gets interesting. In late 2024 and into February of

2025, various corporate indicators were rising, from public company commentary on

earnings calls, the ISM (PMI, New Orders, etc.), surveys about corporate capital

spending, expectations of tax cuts and a return to full bonus depreciation and then…it

all ground to a halt once the tariffs went from a campaign phrase to actual policy. This

started around February 19, was accentuated by “Liberation Day” on April 2, 2025 and

ended up being a drag on corporate decision-making most of 2025.

Just like the stock market hates uncertainties, business decision-makers do not like it when

regulations and policies are in limbo. Between the initial tariff shocks, volatile negotiating

tactics and fluctuating tariff rates and at times an approach that seemed more reactionary

than strategic, corporations slowed their capital spending plans, which had an enormous

impact upon freight creation, i.e., trucking volumes. Plans were paused or shuttered

regarding plant openings and expansions, investments in technology, machines, new offices

and hiring, etc., and this resulted in weak corporate capital spending.

One byproduct was that industrial production (the single biggest determinant whether it’s a

special freight year or an average one or a poor one) never established any momentum.

Indeed, during 7 of the last 15 months IP has been negative. IP is not falling apart, but it’s

been basically running along at mostly a replenishment need for corporations and not

signaling an expansion mode.

The optimism in the January ISM/PMI report is intriguing because it suggests that business

confidence may be increasing. Even if corporations don’t necessarily like where tariffs ended

up, if the shock is over and the rules of engagement are known and stable, then that may be

enough to unfreeze corporate capital spending decisions that had become semi-paralyzed.

Combine that with the low inventories we described previously, and enhanced business

incentives tied to the OBBBA (Trump tax cuts), it is not unreasonable to think that IP and

hence, freight will have at least a modest uptick in 2026.

3) Housing:There are two components to housing, existing home sales (EHS) and new

homes, aka, housing starts or new construction (NC). EHS in 2025 finished at 4.1 million

units, the third consecutive flat year. Some pundits have described the housing market

as ‘frozen’. The good news? During the housing crisis of 2008-2011, EHS never fell

below 4.1 million unit sales and even if they dip slightly in 2026, a dip would likely be

just under 4 million units. And while about 85% of mortgages are at an interest rate

under 5% or less, there are still reasons why people move. From downsizing (often

when they own their home outright) to job or family changes to different housing

needs (new family creation is on the uptick) to job losses and a need to move, there

are myriad reasons why 4 million homes are sold every year.

What’s the Outlook for Interest Rates in 2026?

This is not an official forecast for interest rates; however, we offer some thoughts that are

pertinent to interest rates and hence, trucking volumes.

First, interest rate levels are a function of inflation expectations plus risk requirements. The 10-

year Treasury note is the bellwether for all interest rates and it reflects inflation expectations

plus a required premium for the risk of the issuer. The riskier the issuer then the higher the

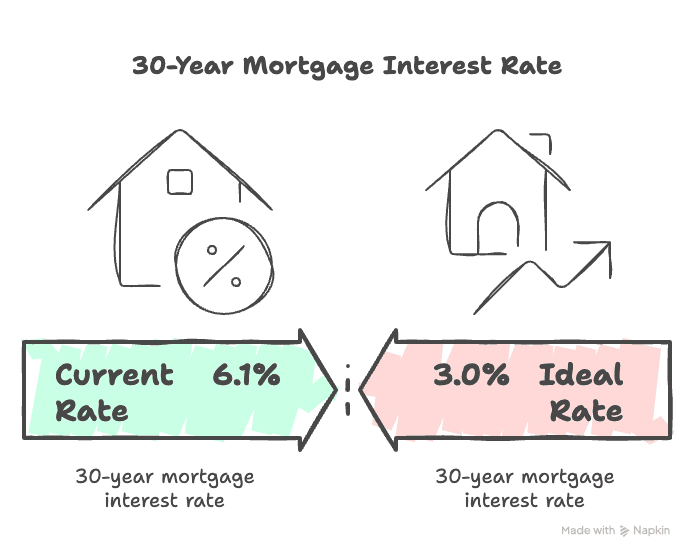

risk premium. Currently, the 10-year Treasury note yield is ~4.1%. Those yearning for 30-year

mortgage interest rates of 2.75% to 3.5% are likely to be disappointed for many years, if not

decades. The current 30-year mortgage is about 6.1% and while it may gradually fall towards

5.5%, it is unlikely to go much lower.

Median home prices nationally have advanced from ~$297,000 in 2020 to over $405,000 last

year. Near-zero interest rates as experienced in the aftermath of the housing crisis

(2009-2015) and during Covid (2020-mid-2022), while fun for buyers, actually have

contributed to the housing affordability problem. Housing costs as a percentage of

disposable income are about 43% (according to the Federal Reserve Board of Atlanta) and

consumer affordability typically peaks around 30% to 33%.

Wouldn’t It be Great if Interest Rates Were Near-Zero, Like in 2021 or 2009-2015?

It would be far better if interest rates come down gradually in 2026-2027 and to levels

nowhere near previous lows. Why? If interest rates fall too low (and too quickly), then

median prices will spike again (up 11% in 2021 and 19.9% in 2022), thereby exacerbating

affordability issues. Between 2008 and 2019 median home prices fell 3 times and were flat in

four other years. While not fun for those wishing to sell, moderating rates of increases in

median home prices will eventually create a healthier home ownership market for all

constituents, one where affordability is improved and the number of prospective buyers

increase for homes listed for sale.

So If Demand is Mixed and Mediocre, Then Will Trucking Supply Be the Story of

2026?

Since mid-2026, trucking headlines have been dominated by topics like ELP (English

Language Proficiency), non-domiciled CDLs, and the upcoming elimination of selfcertification

of CDL schools and instructors.

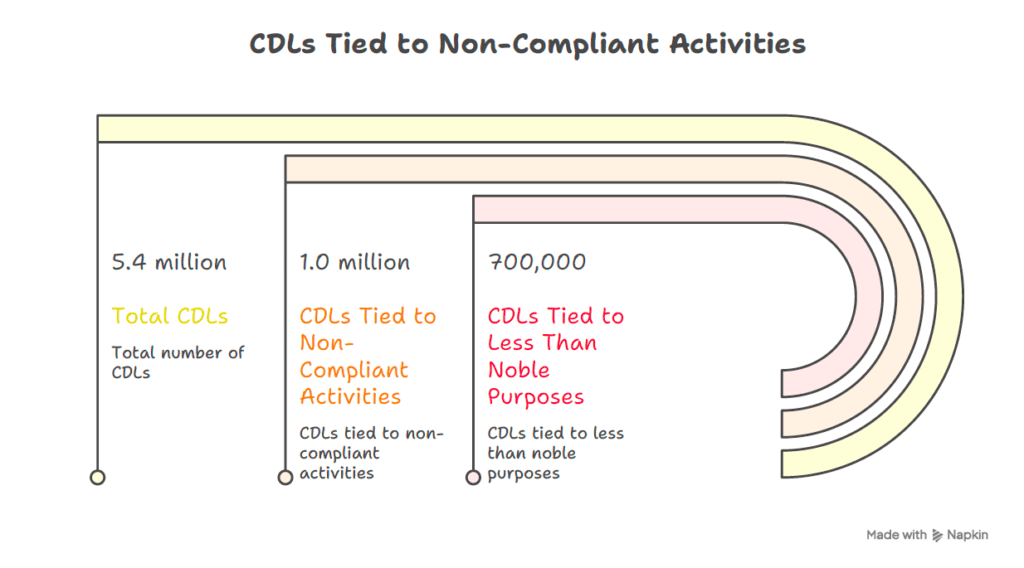

When looking at the number of interstate CDLs (3.8 million) and intrastate CDLs (1.6 million),

then 5.4 million CDLs exist. We have looked at CDLs from numerous issues, including all of

the headline topics of 2025 and early 2026. We have concluded that somewhere between

10% to 15% of CDLs are tied to DOT #s committed to either operating non-compliantly on a

consistent basis or to commit cargo theft and fraud…or both. Our estimates show that slightly

over 1.0 million CDLs may have been tied to such activities (even if the driver was not fully

aware). Due to weak freight rates, many drivers have left the industry, perhaps around

350,000, most tied to not making enough money. That leaves around 700K CDLs tied to less

than noble trucking purposes or about 13%. Even if that figure is high, it is not inconceivable

that at least 10% of CDLs are tied to operators not playing by the same rules as most of the

decent, hard working trucking companies and drivers in the industry.

What Do All of These Numbers and Trends Indicate for 2026-2027?

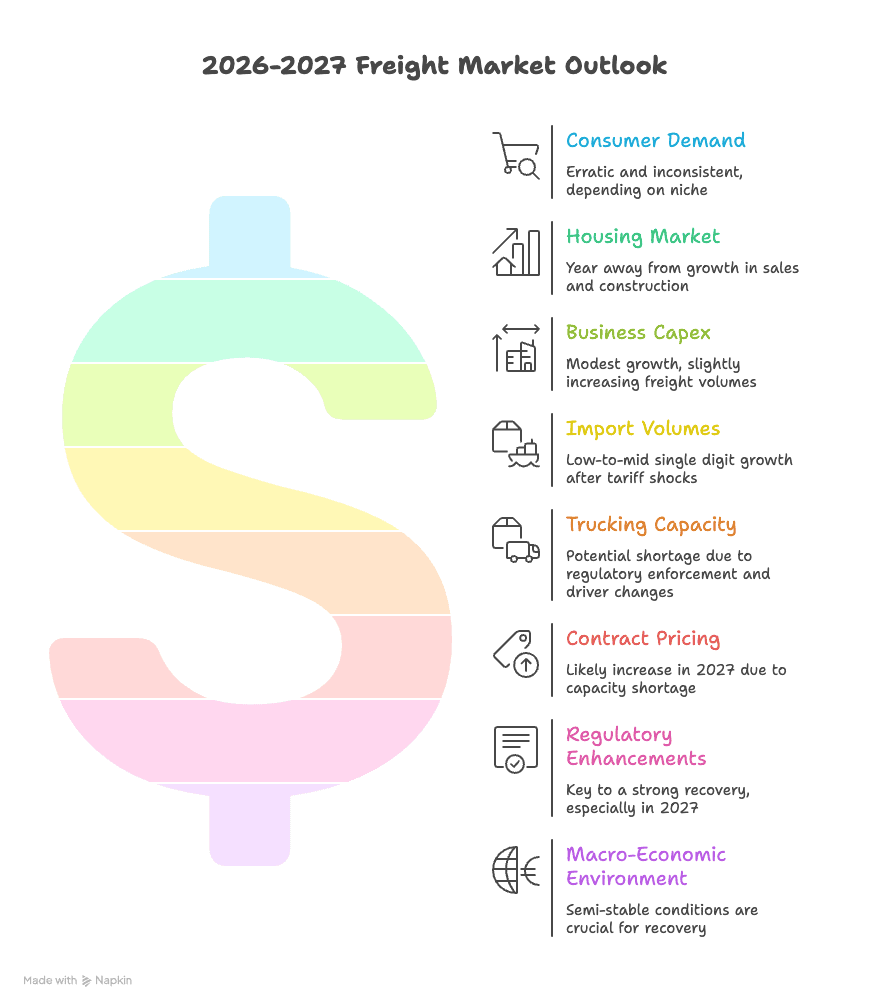

Consumer demand/spending and retail sales are likely to remain a bit erratic and

inconsistent, depending upon the business and consumer niche. Housing is probably a year

away from seeing growth in existing home sales and new housing construction starts. Yet,

business capex is likely to grow modestly in 2026, which would slightly increase freight

volumes. Import volumes, after the tariff shocks of 2025 and a 48% drop in Q2’25 and Q3’25,

are likely to see low-to-mid single digit growth throughout each 2026 quarter.

Entering 2H’2025 excess trucking capacity or supply was likely 2% or less. A 1% drop in

interstate trucking capacity would be about 38,000 drivers and between ELP and nondomiciled

CDLs, combined with other recently announced changes, along with others that

we anticipate, it is not inconceivable that 4% to 5% of industry capacity could be eliminated

before Labor Day, which would lead to a capacity shortage of 2% to 3%. That would likely

drive contract pricing up at least 7% to 8% in 2027 and if our estimates are too low, increases

could be double what we described. The keys, of course, are vigilant enforcement of

existing regulations, more practical insights tweaks to improve regulations by the FMCSA and

a semi-stable macro-economic environment.

If a trucking recovery is defined as growth in mileage utilization and at least modest price

increases, then 2026 should be a recovery year. If regulatory enhancements continue, it is

conceivable that 2027 could be a barn burner.

Thom Albrecht is the Chief Revenue Officer at Reliance Partners, an insurance agency

headquartered in Chattanooga, TN. Reliance works with about 10,000 motor carriers and

about 700 freight brokers. In his career, Mr. Albrecht was also the CFO of a Midwest

truckload carrier and before that, a transportation and logistics analyst on Wall Street for 28

years.